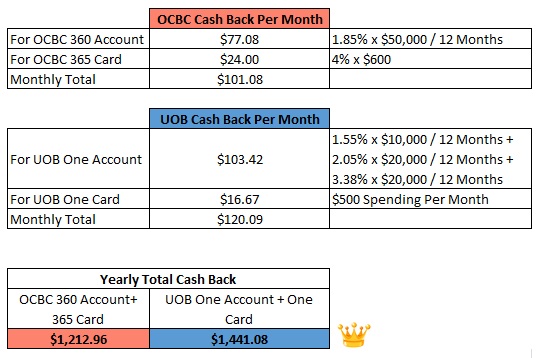

Instead of letting my funds 'sit' idly in the existing current account which doesn't gives any interest, I prefer to let them work harder and make additional 'friends'. The returns can be small but must be practically risk-free.

Having said that, options are not much. The first thing that comes to mind are interest-bearing current accounts and corporate fixed deposits (FD).

I went online to do some comparison work. Surprisingly some foreign banks are offering pretty attractive interest rates for their current accounts and FDs.

Some of the offers are for personal deposit only but I will list it down as well for readers' reference.

For ICBC FD

Validity: Till further notice

Caveat: Not sure whether it's applicable for corporate FD.

For ICBC FD + Current Account

Validity: 31st Oct 2018

For RHB FD

Validity: 31st Oct 2018

Caveat: For personal FD only. Not for corporate.

For CIMB FD

Validity: 31st Oct 2018

Caveat: For personal FD only. Not for corporate.

For CIMB FD + Current Account

Validity: Till further notice

Caveat: For corporate FD only. Not for personal.

12 months FD only Rate: 1.65% P.A.

12 months FD + Current Account Rate: 1.83% P.A. (FD) + 0.78% P.A. (Current Account, Min. S$30k)

I also did a comparison with the upcoming Singapore Savings Bond (SSB) with issue date of 1st Nov 2018.

Again it's not applicable for corporate but just sharing for reference sake.

The offerings from CIMB actually compare favourably with the SSB if I take up the FD + current account bundle. However that might affect my cash flow since a minimum of S$30k has to be maintained in the account on top of the amount that I want to put into the FD.

Readers with extra personal cash wanting to park somewhere for risk-free interest, you might want to consider the FD offered by CIMB. At 1.84% interest, it is slightly higher than the 1.80% from the SSB.

However if you are going for longer tenor like 2 years and more, the SSB is still a more attractive option.