First dividend season of the year. Received dividends from the following:

1) Ascendas REIT

2) Mapletree Logistics Trust

3) Mapletree Industrial Trust

4) CapitaLand Integrated Commercial Trust

5) CapitaLand China Trust

Total dividends received for this 1st quarter amounted to S$2,258.04.

Pretty satisfied as this is slightly higher YoY. Figure for same quarter last year is S$2,003.27.

Per usual practice, all dividends + 50% of my side income are invested back to the portfolio for compounding: the 8th wonder of the world.

This month I've added OCBC @ $16.57 and Venture @ $12.45 to my existing positions.

The OCBC purchase comes with a 5.1% dividend yield excluding special dividend. The group has released a pretty solid FY24 with a 8% increase in net profit and EPS. Final dividend was reduced by $0.01 YoY while CEO Helen's pay when up instead. Not much to complain anyway, just an observation on my part.

The Venture purchase comes with a 6% dividend yield. This was done partly to average down, partly to reduce my REITs concentration and partly as a recovery bet in the company. Their recent results haven't been very encouraging although they are maintaining their dividend amount and they are consistently generating positive free cash flow. Hence I am keeping this counter to a small portion of my portfolio. In fact this is the smallest position at 3.2%.

Interesting bit, after I made the Venture purchase, another counter which I have been eyeing actually fell to my TP. Alas I have already expended my bullets this month so guess this has to wait. If another opportunity arises in April this will probably take precedent. Let's see.

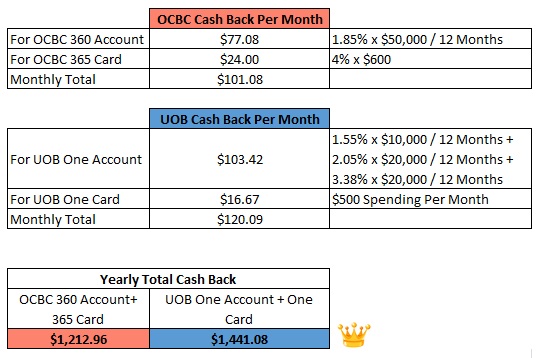

Another important news is regarding OCBC 360 Account. There will be a revision to the interest rates on 1st May 2025. Based on the revised terms, I can probably earn 2.65 - 3.85%. Not fantastic but not too shabby either. Moving forward this will probably be the trend across the banking sector so I won't be in a hurry to move funds around yet.

Revised terms from 1st May 2025 onwards: