So you guys probably already know that OCBC has changed the terms and conditions of its 360 savings account again.

If memory serves me well, this is the 2nd time they have changed those conditions.

Initially it was 1% interest P.A. for each of its original 3 categories. After that it was changed to 0.5% for couple of the categories. Now it's down to 0.3%.

While it is not totally unexpected, it is still disappointing nonetheless.

With the new conditions (interest rates) in place from 1st April 2017 onwards, it would serves us well if we can do an apple to apple comparison with the next closest saving account to see which benefits us most.

With that in mind I did a comparison between the OCBC 360 account and UOB One account.

First off, the difference between the existing OCBC 360 conditions and the new conditions from April onwards.

As you can see, interest rate has dropped in two of the categories while new condition has been set.

Personally I am able to get 2.25% + 1% on incremental saving amount on current conditions. Once the new scheme kicks in, realistically I should be able to get 1.85%.

Now, the interest rates offered by UOB One account.

Interest offered by One account is slightly different in the sense that the rates are on step up basis.

So which is the better account in terms of interest rate for the man in the street?

For this question we do a case study based on two scenarios as follows.

Case Study 1:

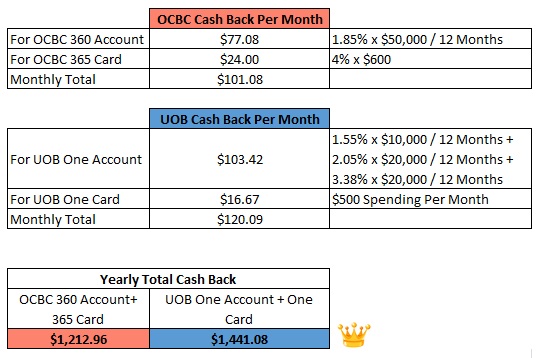

For the average Joe who maintains $20,000 in his account every month and is able to get 1.85% from his OCBC 360 account from April 17 onwards or 2.05% from his UOB One account.

On top of that he also spends at least $600 on his credit card every month. Since the cash rebate for OCBC 365 card is mostly between 3 - 6%, we use a mid figure of 4% for our average Joe.

Case Study 2:

For the richer average Joe who maintains $50,000 in his account every month and is able to get 1.85% from his OCBC 360 account from April 17 onwards or 3.38% from his UOB One account.

On top of that he also spends at least $600 on his credit card every month. Since the cash rebate for OCBC 365 card is mostly between 3 - 6%, we use a mid figure of 4% for our average Joe.

Case Study 3:

For the even richer average Joe who maintains $70,000 in his account every month and is able to get 1.85% from his OCBC 360 account from April 17 onwards or 3.38% from his UOB One account.

On top of that he also spends at least $600 on his credit card every month. Since the cash rebate for OCBC 365 card is mostly between 3 - 6%, we use a mid figure of 4% for our average Joe.

In conclusion, you can see that with a larger savings amount up to $50,000, the UOB One account offers a better deal than OCBC 360 account.

However if your savings amount starts to exceeds $50,000 you might want to take a closer look at the OCBC 360 account since the interest rates are valid up to $70,000 whereas UOB One account only offers 0.05% base interest for savings above $50,000.

(Thanks to reader Vince Chew who pointed this out)

If you are like the average Joe in our case study who maintains a lower amount in his savings, OCBC 360 is probably better for you.

For myself, I will still stick with my OCBC 360 account FOR NOW as most of my funds are currently in investments.

It's not worth the hassle for me to switch my Giro billings.

Furthermore UOB, like other banks, can change the conditions for their UOB One account anytime. So I will adopt a wait and see attitude first.

If you compare both for 70k saving, I believe OCBC still better. Though not many ppl will have that kind of saving. Do you mind to add another case study for that?

ReplyDeleteHi Vince,

ReplyDeleteThank you for your comment. That's a sharp observation.

As you correctly pointed out, for $70K savings OCBC indeed offers better returns.

This is due to the fact that their interests are valid up to $70K whereas the bonus interests from UOB One are only valid for savings up to $50K.

Please see the updated post with case study 3 as requested.

Thanks for working out another case study. I would also stick with OCBC as of now

ReplyDeletecan you compare with BOC smartsaver or Maybank iSavvy?

ReplyDelete